To remotely manage their accounts and active cards, VTB client ...

How to get a loan secured by real estate? Do you issue loans without proof of income? What is a non-target and consumer loan + 3 ways to get a loan with a bad credit history + 3 main risks of a loan secured by real estate.

Credit- a quick way to get a substantial amount for personal needs. Many use the funds received to develop their business or buy real estate.

Every day the lending system is growing and offers all new types of services at more favorable rates for the common people.

Today we will analyze what is a loan secured by real estate and how it should be properly drawn up.

Making a profit from the lending process has been a profitable business since the 2000s. Previously, the need for money was satisfied by banking institutions by 95 - 98%, and now private companies have won about 40% of the financial market for providing credit services.

Low interest rates and debt repayment period are the main advantages of private lending.

Secured loan- the allocation of money to the borrower on the basis of a temporary transfer of ownership of real estate to the service provider.

Real estate has the highest liquidity indicators, so a private house is much easier. The main goal of the lender is to sell the goods as soon as possible in case of non-payment of funds to the borrower, and real estate and values are best suited for this role.

Are you the owner of a private house or do you have a living space in the city? Or maybe you only own the rights to a part of the dwelling? Even this option can be considered by the lender in the event of a disbursement of funds.

Absolutely any housing can act as collateral, but remember, the size of the loan depends on its estimated value. The most popular loan secured by existing real estate is a mortgage.

Mortgage- a type of collateralized loan, where the borrower's private real estate acts as a guarantee.

People intending to take out a mortgage loan expect an amount of 600,000 rubles or more. Banks annually simplify the registration process and, therefore, the growth of mortgages is growing annually and tirelessly.

Differences from a loan without collateral:

An important condition is the presence of the owner's direct rights to real estate, which he is going to exhibit as a guarantor of the return of funds.

If the property value is very low, the decision on extradition is submitted for additional consideration, because of this there is a high risk of refusal.

What to do if the bank refused to provide a loan secured by the existing real estate, we will consider below.

The most common type of lending available to absolutely any citizen of the Russian Federation. Issued in 100% of banks and other organizations related to the provision of lending services.

There are 4 types of consumer loans:

Unsecured is the usual loan of funds for personal non-production needs. If you apply for a loan on the basis of property, then we will come to collateral type. For large amounts, consumers issue target loan secured by real estate.

Specific features of a targeted consumer loan:

This is a convenient method of buying a home, which is analogous to a mortgage loan.

Features of non-targeted lending:

In practice, obtaining a non-targeted loan will take much less time than others. Each bank has its own form of forms and.

The more favorable the conditions, the more information will be required from you.

The interest rate is lower than for conventional consumer lending, and depends on the additional terms of the transaction, as well as the size of the loan.

The age of the borrower must be between 18 and 55 years old, sometimes lenders make concessions and, if there is insurance from the guarantor, they can issue money to persons under the age of 65.

The “non-payment” rule may be canceled early if the issue is resolved early with the representatives of the creditors. Official registration takes place through the client's application.

Came from the West about 7 years ago. Has one of the lowest interest on loan funds, but at the same time requires a large amount of confirmation and other documents from official government bodies.

Most popular with entrepreneurs.

A loan secured by commercial real estate today is issued at the rate of 18 - 22% per annum and for a period not exceeding 5 years. These indicators are associated with the aftermath of the 2014 crisis.

Recently, lenders are returning to rates of 12-15% and to the possibility of obtaining a loan for 10 years.

What factors affect the size of the% rate:

Legal entities or their representatives can receive a maximum of 71 - 73% of the appraised value of commercial real estate, which is provided as collateral.

If the structure is built of wood or according to the documentation there was a change in layout, then the estimated cost is reduced.

What else do lenders pay attention to:

If the commercial space has a layout related to a narrow specialization in use, this can significantly affect the size of the funds provided. The reason is clear: if the borrower is insolvent, the lender will have to sell the property as soon as possible, and in this situation it will be very difficult.

The features of the assessment of commercial real estate include post-assessment site inspection.

The process involves a complete analysis of the premises in search of problem points that can affect the implementation in the future.

A big advantage of commercial lending is the ability to carry out work at the facility, paying not rent, but the cost of the building itself. Among small and medium-sized businesses, such loans have become a real salvation.

The disadvantages include strict requirements for loan processing and real estate documentation.

Compulsory insurance can increase by 10 - 12% the initially expected expenses for the maintenance of such property, if we are talking about a mortgage loan secured by commercial real estate.

The main elements of the agreement consist of 5 points:

Item 1: Submission of the object of the pledge.

The borrower provides documentary proof of ownership of the property. The object may be located not only in the region where you plan to apply for credit funds.

Some banks provide an opportunity to register funds for property located anywhere in the country.

Item 2: Valuation of collateral.

The process is handled by creditors' specialists or an independent qualified employee. The client has the right to hire an independent expert to obtain a more objective assessment.

Most of the organizations that provide loans, prefer to underestimate the appraised value of real estate.

The broker's help will allow you to receive 15 - 20% more funds than with the standard procedure.

Item 3: Choice of the crediting period and the size of the interest rate.

Each financial institution, at its discretion, sets the terms of lending and the size of interest rates.

Mortgage lending is the most profitable in terms of annual interest, but payment terms stretching for 15-20 years can become a problem.

Item 4: Collecting information about the property and the borrower.

Before the direct conclusion of the contract, the system conducts an additional study of your financial capabilities as an individual.

A certificate from the place of work, documentary evidence of the amount of wages and other data that can affect the decision to issue cash resources.

Clause 5: Verification of the permissions that the lender provides for the mortgaged property.

Usually this point does not attract attention in the standard procedure, but this is where the pitfalls can lurk.

Whether it will be possible to dispose of real estate after its announcement as collateral is the most important issue that should be resolved before the end of the lending procedure.

You can only change the property during the application process.

The document is certified by a notary of the company or your personal representative of the notary office.

The advantages of this method made him a leader, and today a loan secured by real estate without a certificate of income can be obtained in every second bank in the country.

The procedure practically does not differ from the standard one. The main nuance is the ability to submit a package of documents without income statement of an individual.

Attempts to obtain such a loan by commercial organizations are close to zero.

A bank making such concessions often includes other credit requirements that can prove the borrower's solvency.

The categories most often resorting to obtaining loans without a certificate of income are low-income families and young families. The intent can be to buy or arrange a home, or to pay other debts owed by the borrower.

Depending on the purpose, it is necessary to focus on targeted or non-targeted consumer loans.

There are unforeseen difficulties that can affect your credit history. This can become a big problem with subsequent calls to banks.

Absolutely all fines are entered into the statistics of debt repayment, even if you are. The result will be a bad credit history.

By requesting funds from the bank, you provide the information that the system requires, without even mentioning past problems. But the bank will still receive the data through its own network.

The previously taken loan was registered with special authorities, and if there were fines, everything was automatically recorded. Particularly unscrupulous borrowers are included in the "black list", to which 95% of the country's banks have access.

There are 3 ways to get a loan secured by real estate with a bad credit history:

Direct contact to the bank.

As bad as your story is, each situation should be considered on a case-by-case basis.

Some banks are loyal to the solution of such issues, and you will have a 20 - 30% chance of getting a loan.

Contacting a broker for services.

Intermediaries can resolve issues with bad credit history within 2 - 5 days, if the reasons for the delay in payment were justified by the situation.

Often, such companies work with 2 - 3 banking systems, therefore, if requests for a loan do not pass, it will be possible to turn to another broker.

Loans from credit firms.

There are more and more private companies that provide an opportunity to get a loan.

Real estate as collateral pays off very quickly in case of non-payment.

The issuance of funds is provided for a period not exceeding 5 years.

To find out the current state of your credit history, send a request to the Central Department. Use the dossier code, as a key, in the future on the website of the Central Bank of Russia to obtain the information you are interested in.

You can find out your credit history for free only once a year, subsequent calls will cost you 400 - 600 rubles.

About 70% of the country's citizens want to get money in their hands when applying for a loan, therefore this issue is very relevant.

Depending on the credit plan, each bank has its own terms of issue, some carry out a wire transfer to an account, while others can issue money in cash.

Features of issuing a cash loan:

The easiest way to get money in cash is to use the offers of commercial organizations. They are not very interested in your dark past, if, of course, there is one, and they are ready to give up to 2,000,000 rubles in cash.

Each case should be considered on an individual basis: the more attractive the property, the more bonuses for yourself you can knock out.

An example of such a resource is mos-zalog.ru

This is a private company that has been providing loans to Russian citizens for 4 years. The main office is located in Moscow, but it is possible to arrange a deal remotely.

Within 5 days, you can receive money to your account. If you take in cash, you will have to visit the branch of the organization's partners to resolve additional issues.

Negative credit history is not taken into account, and the list of documents is minimal. To issue funds in the department of the organization, you will need a passport and another document proving your identity.

As a result, the most significant factor is loan amount It is not so easy to issue 50,000,000 rubles in cash, even for large institutions of the country.

The list of banks in Russia has more than 60 public and private institutions, therefore, you should carefully consider the conditions and quality of processing credit funds.

We took into account the reviews of ordinary users of the country on the main banking website banki.ru, and selected for you lists of the best offers with moderate interest rates for all occasions.

| Best Financial Institutions for Consumer Credit | |

|---|---|

| Housing Finance Bank | The rate is not higher than 13% for a period of up to 18 years and with a loan amount of up to 5,000,000 rubles. There is an additional one-time commission of 5% for personal insurance. |

| Confidence Bank | Loan size up to 12,000,000 rubles for up to 130 months at 12% per annum. If you refuse personal insurance, the interest rate increases by 12 points. |

| Gazprombank | There are 2 options. In the first, the rate is 12% for 12 months, and the amount of funds is no more than 25,000,000. The second allows you to get a loan for 15 years at 13% per annum. |

Almost any banking institution in the country can provide you with a consumer loan secured by real estate on similar terms.

It all depends on your personal preferences and the possibility of contacting one or another bank department.

| The best financial institutions for unearmarked loans | |

|---|---|

| Alfa Bank | If the loan amount is more than 700,000 rubles, the interest rate will be 12%, and up to 250,000 - 26%. The annual size is determined for each case individually. There are no additional commissions, and the maximum period is 60 months. |

| Post Bank | Amount from 400,000 to 1,200,000 at 13% per annum for up to 50 months. There are no additional fees and commissions. The absence of involuntary insurance will be a pleasant bonus. |

| VTB Bank | Interest depends on the terms of the loan - from 15% to 20% per year. The loan amount does not exceed 2,500,000 rubles for no more than 5 years. No insurance is required and there are no additional fees. |

Inappropriate loans are provided by about 50% of all financial institutions.

Due to a number of additional conditions, banks prefer to have information on the spending of the allocated funds.

| Loan without income statement | |

|---|---|

| Moscow credit bank | The loan amount reaches 2,500,000 rubles at an annual rate of 13% to 28%. It all depends on the terms of the contract and the term. There are no additional commissions. If insurance is canceled, 3 points are added to the annual ones. |

| Renaissance Credit | Issuance of funds secured by real estate for a period of 5 years from 13% - 27% per annum to 800,000 rubles. No insurance required. |

| SKB Bank | The rate is 28% for a period of up to 3 years and an amount not exceeding 300,000 rubles. Additional commissions and insurance are not needed. |

Issuing a loan to a consumer without proof of permanent income is a dangerous business, even on the security of property.

The appraisal committee is very strict and the amount of funds allocated rarely exceeds 50% of the market value of the property.

Only 25% of banks in the country practice.

Banks are very reluctant to make deals to issue loans to people with a problematic history of repayment.

Only 4% of the country's banking institutions are ready to provide such services, but there will be so many additional conditions that it will be easier to find an alternative source of financing.

The way out of the situation will be to contact credit brokers or private companies that will help you get a cash loan secured by real estate.

How to get a bank loan secured by real estate?

The answer is given by experts in finance and lending:

Even by borrowing money from a bank, you may be exposed to certain risks.

Of course, if you have a bad credit history or need a loan without a certificate of income, the list of available resources is sharply reduced, but it is rash steps that can cause your financial problems in the future.

What risks await:

Fraudsters' tricks.

By transferring money only on paper, you are pushed to conclude a contract, which states that you, of your own free will, give the property into the wrong hands.

Loss of real estate.

Think rationally. You should not take an unbearable loan, the interest from which will not only not help you solve current problems, but will also add new ones.

Additional expenses.

The interest rate in foreign currency may fluctuate depending on the economic situation in the country.

Even in rubles, you will not be able to insure yourself against the payment of the "Thirteenth Payment".

A personal notary or broker will allow you to protect yourself as much as possible. Property appraisals are also best done with the help of an independent expert, so you can get the most out of the situation and turn it around to your advantage.

A loan secured by real estate has now become a lifesaver for a large number of residents of the country.

However, do not forget that you will spend 5 or more years on its repayment, and the final amount will be with a considerable overpayment ...

Helpful article? Don't miss new ones!

Enter your e-mail and receive new articles by mail

Let's see which banks provide loans secured by real estate. First of all, we note that real estate objects: apartments, houses and land are readily accepted by financial institutions as collateral. Do you know why? Because deals with their participation are beneficial to both parties. To both the borrower and the lender.

The benefits of the former are obvious. A loan secured by highly liquid collateral is provided on more favorable terms than a regular consumer loan. Not to mention loans on one or two documents and express loans.

The second, accepting real estate as a pledge, can be 99% sure that the debt, as well as the accrued interest will be paid in full, because the client pledges his home. Therefore, he will treat the loan as responsibly and deliberately as possible.

Contrary to popular belief, the ownership of an apartment, house or land remains with its owner, that is, the borrower. The consequence of the transfer of real estate as collateral is the imposition of an encumbrance on it. In particular, a bank client who has provided his property as collateral has the opportunity to:

The last action is possible only with the consent of the bank.

But it is impossible to sell or donate an apartment / house until the encumbrance is removed from her / him. This happens after the full payment of the loan taken.

The total amount of funds that banks issue on the security of real estate can reach 80% of its appraised value. However, there are few such offers on the market. In most cases, we are talking about 50% -60% of the real market value of housing. The maximum value of the loan term can be up to 20 years.

The following are accepted as collateral:

The mortgaged real estate, first of all, must be liquid. That is, it can quickly turn into money. This condition presupposes not only its ideal [real estate] condition, but also the demand in the market. For example, a bank is more interested in an apartment for 2.5 million than a luxury apartment for 15 million rubles. Apartments, houses and land 50 kilometers or more from Moscow are considered illiquid. In addition, apartments in old high-rise buildings and old houses are undervalued.

An object pledged by a credit and financial institution must be free of any encumbrances. At least in the part that corresponds to the amount of the loan being issued (but the chances of getting money in this case are greatly reduced). The fact of encumbrance is revealed simply: by sending a request to the Unified State Register of Real Estate (Unified State Register of Real Estate). The resulting extract will describe all claims and encumbrances and list all owners of an apartment, house or land.

This is how the current bank offers for granting loans secured by real estate look like (in alphabetical order):

| Bank | The name of the program | Maximum loan amount | Interest rate | Loan terms | Insurance |

|

Secured by real estate |

from 1 month to 10 years |

property |

|||

|

Bank of Moscow |

Secured by real estate |

from 490,000 rubles |

from 1 month to 20 years |

property, personal and title. If only the first, then +3 p.p. to the interest rate |

|

|

Inappropriate mortgage |

up to 90,000,000 rubles |

from 1 month to 20 years |

property, personal and title. If only the first, then +1 p.p. to the interest rate |

||

|

Consumer secured by residential real estate |

up to 14,000,000 rubles |

from 1 to 15 years |

property, personal and title. Any variations (one of three or two of three) - +3 p.p. to the interest rate |

||

|

Bank Rosgosstrah |

Secured by real estate |

up to 10,000,000 rubles |

from 1 to 10 years |

property, personal and title. Any variations - from +3 p.p. to +6.5 p.p. to the interest rate |

|

|

Rosevrobank |

On the security of an apartment |

up to 15,000,000 rubles |

from 6 months to 15 years |

property, personal and title. Any variations - from +2 to +5 p.p. to the interest rate |

|

|

Rosselkhozbank |

Inappropriate secured by real estate |

up to 10,000,000 rubles |

from 1 to 5 years |

property and personal. If only property, then +1.75 p.p. to the interest rate |

|

|

Russian Capital |

Secured by real estate |

up to 5,000,000 rubles |

from 12 to 180 months |

personal and title. If without insurance, then +5 p.p. to the interest rate |

|

|

Secured by existing real estate |

up to 5,000,000 rubles |

from 13 to 36 months |

property and personal. Variations - +1.5 p.p. to the interest rate. Without insurance - +3 p.p. |

||

|

Secured by real estate |

up to 30,000,000 rubles |

from 12 to 84 months |

property, personal and title. If only property, then + 4 p.p. to the interest rate |

||

|

Sberbank of Russia |

Consumer secured by real estate |

up to 10,000,000 rubles |

up to 84 months |

property |

Despite the lower rates for lending programs secured by real estate, they all have one serious drawback: the borrower, in case of difficulties with debt repayment, risks losing the mortgaged apartment, house or land.

Those who receive consistently high income should be interested in which banks give loans secured by real estate, and this circumstance will continue in the next few years. In this regard, it is necessary to very carefully study the conditions of banks in terms of drawing up an insurance contract. Some insurance companies offer to mitigate the risks of loss of work, health and even life of the borrower. On average, paying insurance premiums increases the interest rate on a product by 3 percentage points. And this again suggests that it is better to calculate your financial capabilities before applying for a loan.

May 28, 2016 8:19 am 27732 0

To date, it is very difficult to get a large amount of credit, it is especially difficult to do it at a reasonable, and not extortionate, as is often the case, interest.

Banks are reluctant to issue a loan secured by real estate without confirmation of income, but, nevertheless, there are several adequate proposals in this industry. We have conducted a thorough analysis of the offers of banks in the Russian Federation and now we present to your attention options for obtaining a loan secured by real estate without proof of income in any region of Russia. Let's start.

So, we will not now argue about whether, in principle, it is worth taking a loan secured by real estate, because in itself, it is of great value, because if you are looking for such an offer, then you have decided everything for yourself, and our task is to offer you the best option.

Naturally, only those proposals will be considered here in which decent amounts of loans appear, otherwise it would be more logical to apply not to a bank, but, say, to.

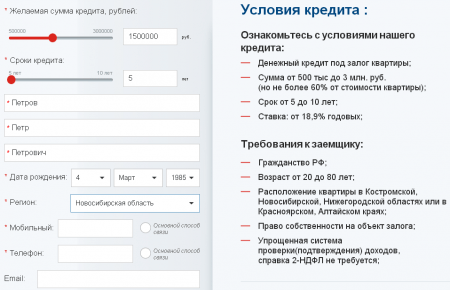

So, few banking institutions offer a cash loan without certificates and guarantors secured by an apartment or other real estate. We will consider both those that do not require such documents at all, and those that are more demanding, but do not drive borrowers into a dead end.

For easy navigation, the list of banks where you can get a loan secured by real estate without proof of income and a minimum of documents:

This loan offer from Tinkoff Bank has many advantages, in particular, there are no requirements for a large package of documents and long waiting lines. As well as:

And the most important thing is that the application leaves without checking the credit history or information about past debts, and Tinkoff does not ask for a certificate of income confirmation. In addition, it is not even necessary to provide documents on the property! The whole transaction is drawn up practically according to the passport on the day of application.

The bank offers a solid option for obtaining a loan secured by real estate without income certificates, with obtaining a decision on obtaining a loan online! With a very low interest rate, from only 11% per annum, which is one of the best offers at the moment On the market.

Once again, we draw your attention to the fact that you will not be required to confirm income certificates, 2-NDFL forms, 3-NDFL forms, certificates from relatives and the rest of the bureaucracy, and the package of documents required to obtain a profitable loan secured by an apartment is small.

Housing Finance Bank(BZD) has been on the lending market for several years and has managed to establish itself as a reliable player in this area. BZD is a specialized mortgage bank with a high level of capital adequacy, which has been actively working in the Russian mortgage lending market for more than 24 years.

Priority areas of activity:

The maximum amount that can be counted on for a loan secured by real estate is 20.000.000 rubles, minimum - 1.000.000 (up to 70% of the cost of the object). Loan term from one to 20 years.

Leave a request onlineNaturally, the largest bank in the country has such a popular option in the list of programs, which is provided here on quite acceptable terms.

So, you can get a non-targeted loan secured by real estate in Sberbank on terms of an interest rate of 13%, for a period of up to 20 years and for an amount of up to 10 million rubles. But, of course, this is not so easy to do, since the bank makes a number of requirements for borrowers.

In particular, it is necessary to know exactly the market value of the mortgaged real estate, indicate the current level of income, marital status, average monthly expenses, etc. Apart from the standard fields with the required amount and the period during which it is planned to repay the loan.

At the same time, the preconditions on which a loan will be provided in case of approval of the application for its receipt can be seen immediately by filling out a questionnaire on the bank's website.

In general, this is a good offer, but in order to get a really serious amount, it is necessary to meet all the indicators declared by the bank, which is not always obtained.

Looking ahead, I will say that it was this proposal that seemed to our team to be optimal and most acceptable among all the above options, which is why we took it into a separate item.

It is one of the optimal solutions, first of all, because Orient Express almost ideally fits into the title of this review, issuing loans for large amounts using a simplified system, without income certificates.

What are the requirements for a borrower from Orient Express Bank:

Documentation:

The most interesting thing is that in some cases it is possible to provide a loan without proof of income! All you need to do is fill out a short form on the bank's website and

The conditions of this bank are, in general, similar to the previous one. All the same 10 million maximum amount for a period of up to 10 years, however, the minimum rate is slightly higher and is 16% per annum if the loan is taken for a period of up to 3 years inclusive, and 17% for longer loans. At the same time, an additional 3.5% per year can be charged if the borrower refuses life and health insurance during the term of the loan repayment.

But, the lending rate can be reduced by 0.5% if you are a payroll client of the Russian Agricultural Bank.

You can see the preconditions for a loan, as well as assess your compliance with the bank's requirements, on its official website by filling in several fields of the questionnaire.

There you can also apply for a loan online, but, of course, you will have to visit a bank office to get it.

Yes, an additional function for borrowers is the ability to choose the method of repayment of the loan: annuity (fixed constant) and differentiated payments, when the amount will decrease every month.

This bank offers loans to individuals for up to 3 million rubles, and for a period of up to 5 years. Yes, this is less than in the previous versions, but here it is possible to get a loan for a very significant amount without real estate collateral (it is better to discuss this with the bank representatives).

The minimum interest rate here is 16.9% per annum, but with an increase in the amount and term, it grows, as elsewhere, however.

At the preliminary stage of calculating the loan amount and interest on it, a potential borrower does not need to indicate the level of income, place of work, etc. All this is indicated at the time of filling out the questionnaire, or it is negotiated with the bank representatives personally, which, in principle, plays into the hands of borrowers. Perhaps on the spot you will be offered a better program or conditions.

You can find out the preliminary amount, as elsewhere, on the official website.

Later, at the time of filling out the application, the bank will request information about you and your financial condition.

In general, the offer is interesting, if you do not need a very large amount, then it will be somewhat easier to get it from the Bank of Moscow than in the previous options.

We can say that all three sentences described in the section do not differ so much from each other. Perhaps the most significant difference here is the requirements for the borrower, which are lower in the Bank of Moscow, but you need to look at the interest rate, knowing your possibilities in terms of income level and the estimated term of the loan.

Another bank ideally suited to the topic of this article and considering applications according to a simplified scheme.

At the same time, the conditions under which lending is carried out are not worse than those that we saw earlier. Yes, the minimum interest rate is higher here - from 11.9% to 22.9%, and the maximum amount is 30 million rubles. But loans are issued for the same period of up to 10 years on less demanding conditions.

You can fill out an application on the bank's website, while specifying in it only the required amount and its maturity date, as well as your contact information: full name, date and year of birth, as well as the region of residence. Questions about income are not asked here (at least, on condition that a loan is issued secured by real estate).

Yes, as you can see, the conditions for obtaining are limited by the location of the property, so not everyone will be able to get a loan. But, if it suits you, try it. The approval rate of applications is higher here than in other organizations.

Not so long ago, a new player appeared on the market of lending, mortgage and collateral loans - the National Mortgage Factory. This is a new player from the "Region" group of companies specializing in the mortgage lending market in Russia. By the end of 2018, the NFI plans to scale the business model by forming a federal business network of “electronic mortgage business”.

"Mortgage Factory" provides such services as:

We are talking about amounts up to 25 million rubles, transactions are made out in a day no commissions.

Let's take a look at the conditions and profitability of this type of lending to citizens.

Today, everyone can find themselves in an awkward position when a large amount of money is urgently needed. What to do in this situation? As a rule, a consumer loan is issued at considerable interest rates. Consequently, it becomes necessary to take a loan secured by real estate: the overpayment is much less, the real estate actually remains in stock, and the funds are issued within a few days. Is this really so, we suggest you figure it out further.

Today, banking institutions provide loans secured by real estate to almost everyone who applies to them. The reason for this is the guarantee of repayment of debt and accrued interest. In the event that the borrower stops paying off the loan, then after the end of the court proceedings, the mortgaged property becomes the direct ownership of the lender. Further, he has the right to use this property exclusively at his own discretion: rent, sell, etc.

In accordance with the legislative framework of the Russian Federation, in order to obtain a loan in a banking institution, the following objects can be mortgaged:

Mortgaging property that is jointly owned is possible only with the consent of all owners. However, for example, a part of the property belonging to the borrower can be formalized as collateral without the consent of other persons.

List of real estate objects that are not subject to registration as collateral:

The main requirements for a bank loan secured by real estate are:

A banking institution necessarily takes into account the liquidity of the collateralized property through a special expert assessment. The bank may not accept the pledge, provided that the potential client provides the only housing in which his entire family and children live, who have not reached the age of majority.

As you know, small loans, up to 100,000 rubles, are often issued by banking institutions without collateral. However, someone who has a negative credit history cannot hope to get an unsecured loan. Therefore, if the client has a bad credit reputation, then the provision of real estate collateral is the only way not only to get a bank loan, but also to significantly raise your credit rating.

As you know, small loans, up to 100,000 rubles, are often issued by banking institutions without collateral. However, someone who has a negative credit history cannot hope to get an unsecured loan. Therefore, if the client has a bad credit reputation, then the provision of real estate collateral is the only way not only to get a bank loan, but also to significantly raise your credit rating.

It should be noted that not all potential borrowers are able to obtain a loan secured by a collateral with a negative credit reputation. In this case, a positive decision directly depends on the rating, that is, banking specialists consider the degree of violation of the loan agreement.

Borrowers who have systematically delayed should not wait for bank approval. If the delay in repayment of the loan was of a one-time nature, the likelihood of a new loan or refinancing of an existing one is quite high. Banking institutions are interested in the timely return of credit funds, therefore, they give priority to collateralized refinancing options.

The quality of the collateral is also important.... So, initially the liquidity of the collateral object is assessed. Of course, the higher it is, the more chances the borrower has to get a loan on favorable terms.

In addition, the client must be prepared for additional costs, since the bank has the right to require compulsory insurance of the pledged property. The purchase of an insurance policy is carried out annually, and its cost is calculated as a percentage of the total amount of the balance of the loan debt.

Today there is a practice of issuing loans secured by real estate without providing a certificate of income. But, unfortunately, not all banking institutions are willing to take such a risk. This is primarily due to the fact that banks do not want to incur significant losses from the potential insolvency of the borrower. Usually, the issuance of such a loan is carried out in an amount not more than 50% of the total cost of the collateralized object.

Today there is a practice of issuing loans secured by real estate without providing a certificate of income. But, unfortunately, not all banking institutions are willing to take such a risk. This is primarily due to the fact that banks do not want to incur significant losses from the potential insolvency of the borrower. Usually, the issuance of such a loan is carried out in an amount not more than 50% of the total cost of the collateralized object.

After the client provides a complete package of documentation, the bank will be ready to make an appropriate decision. Further, a loan contract and a pledge agreement are concluded. The borrower is advised to carefully study all the nuances of lending immediately before signing a formal agreement.

Particular attention should be paid to the following points of the loan agreement:

Additionally, the bank may require to take out health and life insurance of the client. Of course, this will require certain financial costs.

Today, in the modern financial market there is a huge number of credit and microfinance institutions that are ready to provide loans secured by real estate on convenient terms of service. Nevertheless, the borrower is obliged to competently approach the solution of this issue, soberly analyzing his financial situation and comparing it with the possibility of repaying credit debt in the future.

If a person urgently needs money, but there is nowhere to take it, then banks offer a service such as a loan secured by real estate, which provides the borrower with an opportunity to receive a large amount for a variety of purposes, from purchasing an apartment to the opportunity to make repairs at home or relax. Such products are popular in the banking environment, since the bank will protect itself from risks by issuing money - if a loan secured by real estate ceases to be paid, then the property is simply taken away from the applicant.

In connection with the expansion of the market for the construction of personal housing, banks have become more and more willing to lend money secured by real estate, offering them to their clients when the latter do not have the funds to buy a new home, or there is an uncovered difference between the price of an old home and a new one. Even if the clients' goals do not relate to mortgages, banks still go for lending if a person provides housing or any other product that is in demand on the market as collateral.

For the law, a targeted loan secured by real estate is equivalent to a mortgage, because it doesn't matter whether you buy a new home, taking money for this purpose, or taking funds for other purposes, mortgaging real estate - such a loan is considered targeted. There are options when a person, wishing to improve his living conditions, wants to borrow money from a credit institution, pledging real estate that he already has. The contract specifically prescribes conditions that assume that a person will spend the funds received exclusively on the purchase of housing.

Many large banks, for example, Sberbank, offer a non-targeted loan secured by an apartment, which provides that the money provided to the applicant can be spent in any way, and he will not need to provide reports on this matter. Such products of Sberbank should be popular among customers, however, the need to collect many documents, one transfer of which takes two sheets, and the likelihood of not receiving money at the same time, discourages potential applicants.

If a person does not have an apartment, which, according to the documents, is his property, then many banks, for example, Rosselkhozbank, offer to take out a loan secured by a land plot if it belongs to a potential borrower. It is desirable that the site is located in a good area, there are some buildings on it, so that the bank has the opportunity, in case of delay in payments on borrowed funds, to sell it easily and profitably.

Credit companies can accept any property as collateral for a loan, issuing consumer loans for it - it can be cars, trucks, special purpose vehicles, truck cranes, excavators, even antiques, although in this case banks are reluctant to consider such collateral, since antiques require independent assessment, and then selling them is not so easy.

Unlike other bank loan products, the advantages of a loan secured by real estate are obvious:

Each bank has its own interest rate for a loan secured by a house or apartment. There is one common unwritten condition - the fewer documents the client provides to the credit institution, the higher the interest on borrowed funds will be. So, in Sberbank it reaches 14% per annum in rubles, the capital branch of Alfa-Bank offers loan seekers in Moscow 12.5 - 12.9%, from Rosselkhozbank the rate depends on how long the client takes the money - the longer the repayment period , the higher the payment amount will be.

Every person wants to get borrowed funds as soon as possible, without collecting a heap of certificates. It is possible to take out a loan secured without a certificate from Sberbank, only by receiving wages regularly on the card of this bank, or exclusively for educational purposes, for which Sberbank has a special product "Educational". Sovcombank, Vostochny Express Bank and Rosselkhozbank can provide loans without salary certificates, offering the most suitable conditions for borrowers.

Each bank has its own conditions for obtaining a loan secured by real estate, however, the most important requirement is to provide reliable information on the dwelling in its possession, which is supposed to be mortgaged. Its cost is estimated by experts. Based on this, a decision is made to issue the required amount of money, which is a certain share - from 60 to 85% - of the market price of an apartment or house. Banks may impose other conditions regarding, for example, the consent to a loan of people living with the loan applicant.

To simplify the issuance of funds and quickly take out a loan secured by real estate, you must first evaluate and insure your home so that the bank employees themselves do not have to carry out this procedure. In this case, it is necessary to use the services of reputable companies, the documents of which will have weight for bank employees. When filling out the form for the issuance of a particular type of loan, you need to be aware that you will not be given an amount that will be greater than the one stated in the appraisal sheet.

In this case, all costs are borne by the potential borrower and are not compensated in any way. The client submits an application for the type of credit encumbrance required by him in a unified form, then waits for the bank employees to check the documents provided to him for the truth and accuracy. All this takes a certain amount of time - in some cases, consideration of the application takes several hours, sometimes - several days.

When contacting a particular organization, the client should know what documents he will need to apply for a loan secured by an apartment. In each individual case, the situation depends on the banking structure and what product the potential borrower wants to use. When mortgaging housing or any other liquid real estate, the following papers are required:

On the territory of Russia, there are practically the same requirements of the bank for a potential borrower who wants to get money by mortgaging a house or apartment:

After the banking structure has approved the application for a loan secured by real estate, the borrower is given the required amount in cash or by transfer to the account specified by him. The applicant must carefully study all the clauses of the agreement regarding the repayment of the loan body and interest, because if he delays at least three times or does not fully repay the current debt, the pledged property can go to the lender without any legal proceedings.

For simplicity and convenience of tracking payments, banking structures provide for the repayment of a loan secured by an apartment in equal installments, calculating the monthly required amount for repayment and attaching this calculation to the main agreement. The contract indicates the deadline for the payment of the required amount, after which penalties for delay will be calculated. Sometimes there is a possibility of a one-time repayment of the entire debt, in one payment at once, however, this method of quick payment of the loan may be subject to a commission.

All credit and banking organizations are interested in having their funds in circulation and making a profit with the lowest risks. The most popular banks that provide secured loans are Sberbank, VTB 24, Alfa-Bank, Raiffeisenbank, Rosselkhozbank (which prefers to lend to farmers and owners of private household plots), Sovcombank, Gazprombank, IIB, Vostochny Express Bank. Each of them has its own products offering different options for lending with real estate collateral.

Like any loan encumbrance, there are pros and cons of a loan secured by real estate. The advantages include the fact that credit companies quickly and positively respond to the applicant's application, if it is correctly executed and all the necessary documents are attached to it. The downside is that you have to collect and draw up a lot of papers, and then sometimes wait a whole week, whether the application is approved or not.

Found a mistake in the text? Select it, press Ctrl + Enter and we'll fix it!

Targeted lending programs are one of the promising areas of activity ...

Many people have at least once in their life faced a situation when contacting a bank ...